The Bitcoin White Paper Series

The Bitcoin White Paper Series

#3 - Section: Transactions

Evolutionist,

We continue our examination of the Bitcoin White Paper, released by Satoshi Nakamoto in October of 2008, focusing on section two, Transactions.

Let’s say you are out running errands for the day with $200 in your checking account. As you swipe your card at the grocery store, gas station, dry cleaners, etc., the issuing bank keeps track of all your transactions and deducts accordingly from the $200 balance. They make sure you don’t double spend and keep track of your running balance.

The merchants around town are also happy to receive you. There is no need for them to know your account balance as long as the transaction is approved. The merchant pays the credit card processor up to 3% per swipe to provide “trust” to the transaction. The merchant then receives their money in the future once all funds have been settled.

Satoshi wanted to fix the “trust” issue by removing the middleman, in this case, the financial institution collecting 3%. All transactions would have to be public records and kept in chronological order to prevent a double spend. Using a system of digital signatures and hashes, computers on the Bitcoin Network keep track of all transactions and verify the chain at every transaction to ensure no double-spending occurs.

Next week we discuss what this chain looks like, blockchain, or as Satoshi called it, a timestamp server.

To the moon!

Bitcoin: A Peer-to-Peer Electronic Cash System

Transactions

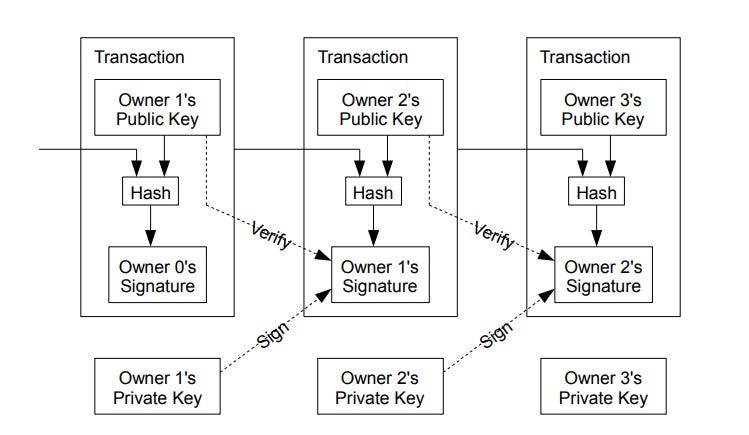

We define an electronic coin as a chain of digital signatures. Each owner transfers the coin to the next by digitally signing a hash of the previous transaction and the public key of the next owner and adding these to the end of the coin. A payee can verify the signatures to verify the chain of ownership.

The problem of course is the payee can't verify that one of the owners did not double-spend the coin. A common solution is to introduce a trusted central authority, or mint, that checks every transaction for double spending. After each transaction, the coin must be returned to the mint to issue a new coin, and only coins issued directly from the mint are trusted not to be double-spent. The problem with this solution is that the fate of the entire money system depends on the company running the mint, with every transaction having to go through them, just like a bank.

We need a way for the payee to know that the previous owners did not sign any earlier transactions. For our purposes, the earliest transaction is the one that counts, so we don't care about later attempts to double-spend. The only way to confirm the absence of a transaction is to be aware of all transactions. In the mint based model, the mint was aware of all transactions and decided which arrived first. To accomplish this without a trusted party, transactions must be publicly announced [1], and we need a system for participants to agree on a single history of the order in which they were received. The payee needs proof that at the time of each transaction, the majority of nodes agreed it was the first received.

[1] W. Dai, "b-money," http://www.weidai.com/bmoney.txt, 1998.

Blockchain: A public list of all blocks mined, ensuring everyone knows which bitcoins belong to whom.

READ 📚

The Bitcoin Standard: The Decentralized Alternative to Central Banking

The Fiat Standard: The Debt Slavery Alternative to Human Civilization

21 Lessons - What I've Learned from Falling Down the Bitcoin Rabbit Hole

The Blocksize War: The battle over who controls Bitcoin’s protocol rules

The Price of Tomorrow - Why Deflation Is the Key to an Abundant Future

WATCH 📺

Cryptopia - Bitcoin, Blockchains, and the Future of the Internet

Bitcoin: The End of Money as We Know It

Banking On Africa - The Bitcoin Revolution

LISTEN 🎤

🔥🔥SUBSCRIBER PERK 🔥🔥

All evolutionists will receive a free digital copy of my upcoming book: title and release date set for Q3 of 2022.